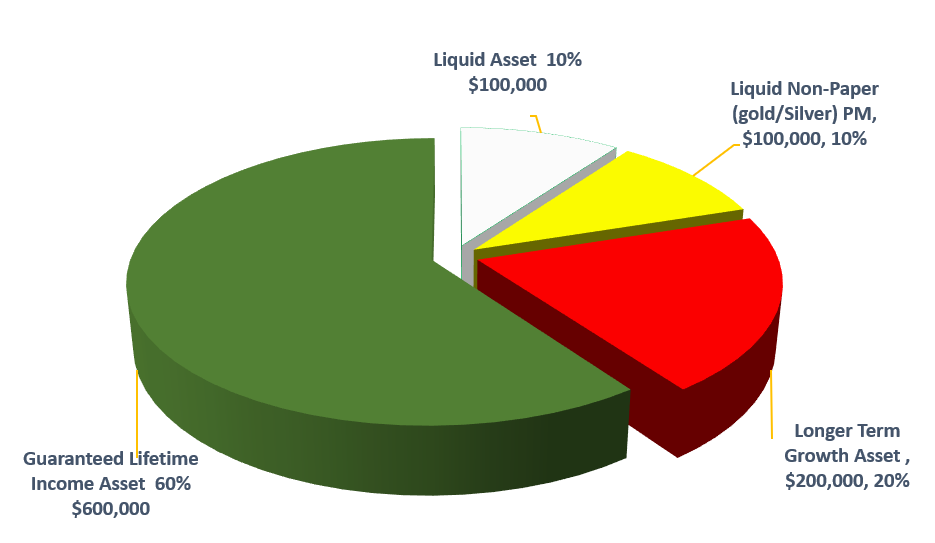

The Retirement Red Zone

The “buy-and-hold” strategy is predicated on one very important principle: The market must return to new highs.

But what if that is not the case? What if a bear market (one that goes down) were to last for is 15-20 years? Does a traditional “buy-and-hold” strategy work in that environment?

Well, let’s take a look. Let’s consider the world’s third-largest economy behind the United States and China – Japan.

Well, let’s take a look. Let’s consider the world’s third-largest economy behind the United States and China – Japan.

Japan’s leading stock index, the Nikkei 225, hit a high of 39,900 in December of 1989. As of early 2021, over 31 years after it touched its all-time high, the Nikkei 225 index stands at just 28,966 – still 27 percent below its closing high over three decades ago!!

10 years ago, the Nikkei was trading at just $9,400, or about 76% below its all-time highs…after 21 years! As of early 2021, over 31 years after it touched its all-time high, the Nikkei 225 index stands at just 28,966 – still 27 percent below its closing high over three decades ago!! So, how did the “buy and hold” strategy work for those Japanese investors who placed their money in the market back in December 1989?

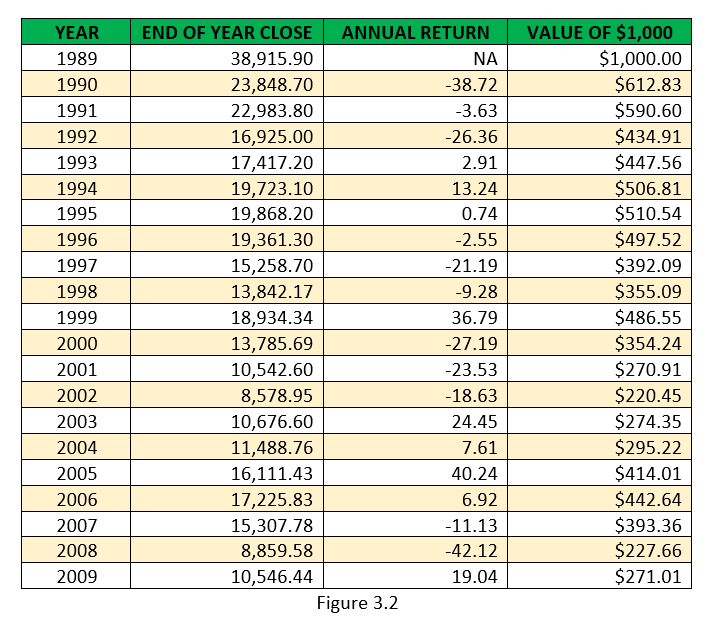

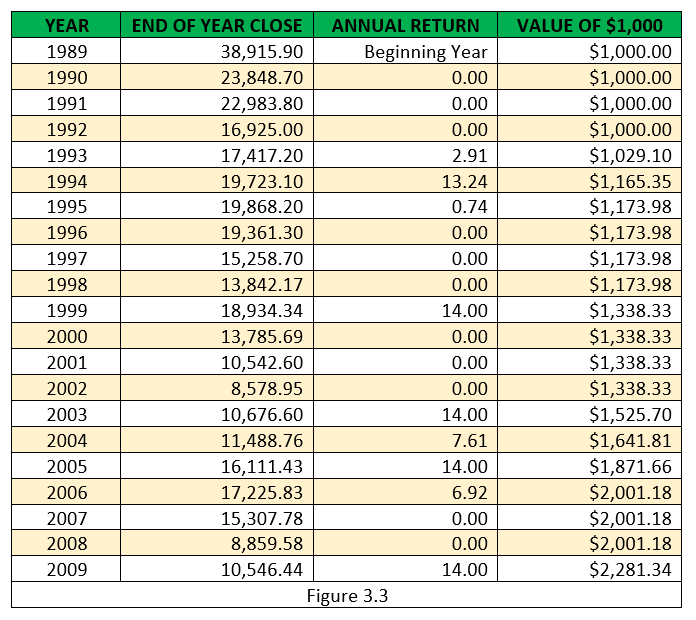

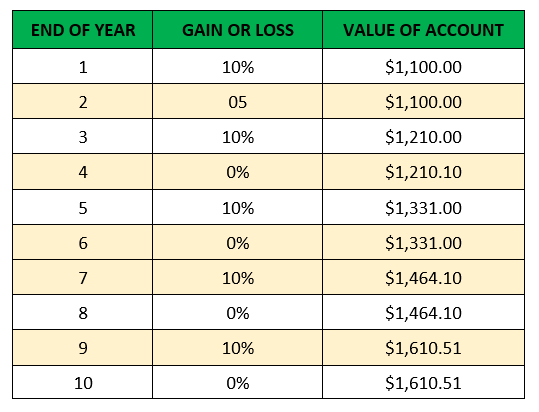

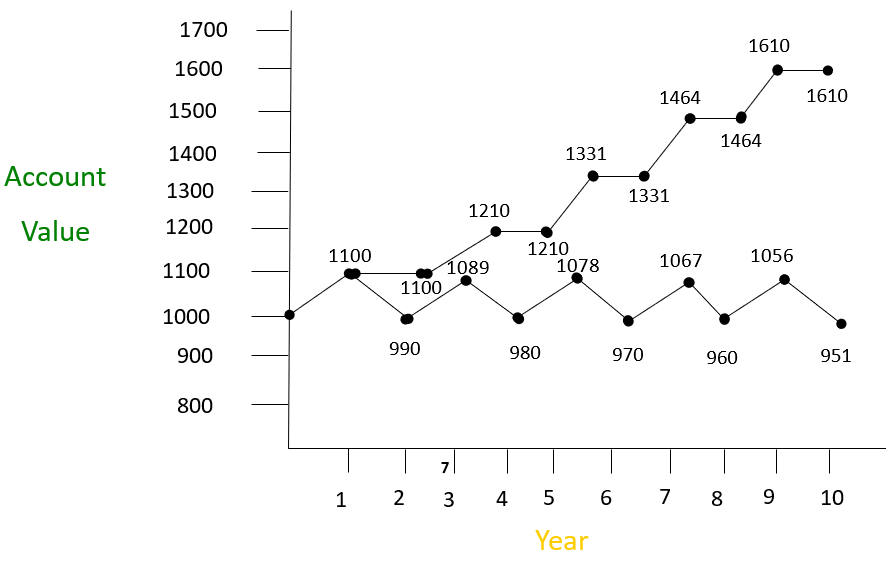

Let’s look graphically at what Patrick Kelly’s book showed us in terms of what $1,000 would have been worth each year, over those first terrible 20 years, from 1989 through year-end 2009 (if it had simply been left in that market, tracking the Nikkei 225 index).